DeFi On Chain Fund

DeFi On Chain Fund

The growing variety of assets on the blockchain brings more diversified portfolio targets to DeFi on-chain funds.

Author: Ryan C @ryanciz233, iZUMi Research

Summary

Compared with the opaqueness of CeFi, DeFi on-chain funds enable a more efficient and transparent asset management model.

With the maturity of decentralized exchanges, lending protocols, and various other derivatives platforms, DeFi on-chain funds have sufficient investment targets, and have the feasibility for wide adoption. Through customized smart contracts to set the scope of operation, multi-signature combined with role delegation, as well as automated algorithms for auto-adjustments, DeFi on-chain funds are well equipped with the advantages of security, transparency, and efficiency. Although right now the overall asset under management (AUM) for on-chain funds is still relatively small compared to TradFi, especially for actively managed funds, this sector will definitely have a huge growth potential in the future.

The growing variety of assets on the blockchain brings more diversified portfolio targets to DeFi on-chain funds.

The emergence of new on-chain assets and derivatives such as LP (liquidity provider) tokens, power perpetual multiplier, and perpetual pools, have brought more composability to DeFi on-chain funds and enabled diversified hedging and risk diversification, providing users with safe, transparent, and balanced risk and return financial products.

There is a clear trend to lower user entry barriers and package complex financial products into user-friendly ones

During the investigation, we observed a clear trend that platforms such as DEXs began to build their own asset management products with user-friendly, easy-to-understand interfaces, - making no requirement for users to constantly operate/adjust. Examples are the USDC vault built by Umami Finance, and the Crab strategy by Opyn.

Funds’ security still needs to be verified. Decentralized wallets will be the ideal entry

Similar to the logic of Web2 financial brokerage applications, advertising fund products on the wallet’s front page is a logical trend. It’s a traffic and funding channel for the fund, and a way for the wallet to gain a revenue stream rather than just relying on the old way of sending transactions to extract fees. But for wallet users, the safety of their fund is critical. The transaction scenario is a one-time scenario, either use it or leave it, and as long as there are no problems with the transaction process, the wallet has no responsibility. The on-chain fund products, on the other hand, are seriously hazardous once a safety accident occurs. The sector as a whole is currently in its infancy, so more time is needed to verify product security.

Intro

Crypto market is always full of risks and opportunities that we can not imagine. Just several months ago, the value of LUNA, one of the top ten cryptocurrency projects with hundreds of billions in market cap, dropped to almost zero within just one week in May, and then triggered a devastating butterfly effect in the crypto industry. Institutions such as Celsius, 3AC, Babel Finance, BlockFi, etc. were impacted, with millions of investors and hundreds of billions dollars involved. The essential reason is the lack of regulation in the cryptocurrency investment space and the opaque asset positions of the various companies underneath, as well as the constant leases and loans among institutions in an optimistic market.

Leverage builds up outside the regulatory framework, and risk also accumulates behind the scene. LUNA eventually became the trigger, and lit the flame of storms. This time the storm was so huge that even some old centralized exchanges, for example, Hoo, which has been through two waves of market circle, got endangered. The reasons for this huge crypto market crash were basically similar to the financial crisis in 2008, though affected a smaller range.

In this research, we will start with the history and basic information of the fund management industry in the traditional financial field, to discuss and analyze a section that has not yet been popular in the DeFi world — DeFi on-chain fund/asset management.

We’ve collected nearly 60 relevant projects from the market, classified, filtered, and selected 22 projects that met our definition for analysis. We list all the summaries about those projects, and give an in-depth analysis of three ones that are worth a deep delve. Now, let’s start with the traditional ones.

Brief Introduction of Traditional Funds

No matter who you are, you can name a few familiar funds. However the "fund", a form of operation that concentrates small, mass investors into large funds, actually appeared two hundred years ago.

The emergence and prosperous development of new things is often required to meet the needs of their times. The essence of finance is to enhance the efficiency of capital utilization, and the origin of funds as a social financial management tool that can achieve more efficient resource allocation is also derived from the demand for capital brought about by the development of real economic situations.

In the nineteenth century, England had just experienced the first industrial revolution, with significant productivity development, colonies and trades all over the world, and rapid wealth growth. The public investors heard similar myths, but suffered from their own lack of knowledge and understanding of the overseas investment environment, so they had the idea of entrusting their capital to relevant professionals to operate and manage. At the same time, some businessmen and seafarers had enough relevant experience but lacked financial support. In 1868, the British government supported this idea by setting up an investment company called “Overseas and Colonial Government Trust”, and entrusting specialized financial experts to invest on their behalf, so that small and medium-sized investors could share the benefits of international investments.

Funds originated in the United Kingdom, but the most rapid development took place in the United States. After World War I, the U.S. economy grew rapidly, moving from a capital-importing country to a major capital-exporting country. In 1926, the Massachusetts Financial Services Corporation of Boston established the "Massachusetts Investment Trust Company", which became the first modern mutual fund in the United States. In the 1920s, the U.S. fund industry grew too rapidly, with assets growing at more than 20% per year, even exceeding 100% in 1927, followed by the Great Crash of 1929.

After the crash and the impact of the Second World War, the U.S. government has formulated comprehensive regulations such as the Securities Act, the Securities Exchange Act, the Investment Company Act, and the Investment Consultant Act, which laid a solid foundation for the development of the U.S. financial industry.

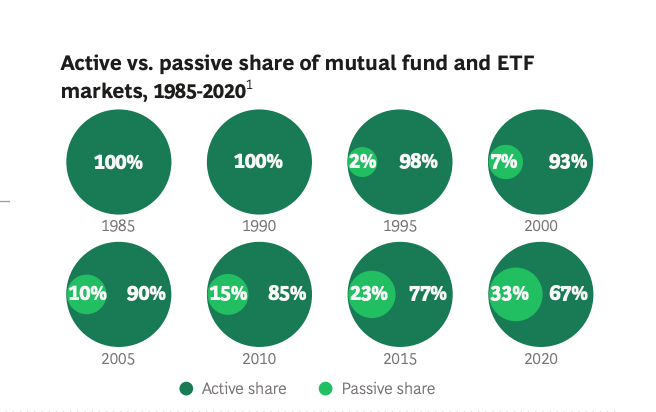

With the continuous development and refinement of the financial system, the fund, otherwise known as the asset management industry, has flourished as time went on. As of 2021, asset management (funds) has become a trillion-dollar market, and in recent years, its annual growth rate has reached as high as 12 %.

And the share of passive investment has grown rapidly, reaching ⅓ of the whole fund market in 2020, indicating that investors have an increased preference for passive wealth management, which can diversify risks through portfolio strategies.

Why do funds get popular?

The funds collect capital from small investors by selling shares and form independent properties. The funds are managed by fund custodians, and the fund managers manage and use funds to conduct investment in the form of investment portfolios. It is a collective investment method that shares benefits and risks. Several reasons for why funds get popular are as follows.

One point is that the fund broadens the investment channels for small and medium investors. It operates the fund through experts, and helps many small and medium investors make portfolio investments. By converting savings and idle assets into an investment, the funds release social resources and provide impetus for industrial development and economic growth. In this process, investors earn the investment income, fund managers earn performance-related income, and the whole society activize idle capitals.

In addition, through the operation and management of professional investors, the development of mutual funds is also conducive to the stability and development of the financial market. Generally, professional investors focus more on long-term strategies and enter and exit less frequently, thus reducing the volatility of the securities market. Likewise, stabilizing financial markets will create a more stable and predictable financing environment for companies.

As a new asset genre, crypto assets have reached a market value of over 1000 trillion dollars in just around ten years. Regarding the management of crypto assets, there has also been a completely different way from the traditional one. At present, most of the crypto assets are still managed via traditional methods, and management of the system is composed of the current legal system, regulatory organizations, and assessment agencies.

However, based on the decentralized, permissionless blockchain network and smart contract technology, a more efficient and transparent fund operation method has been continuously explored in recent years. They use code as the law, remove middlemen, and combine emerging on-chain assets to provide more efficient, less risky, and more diversified financial products.

DeFi on-chain funds

DeFi applications have quickly imitated traditional finance in just five years since the emergence of Ethereum and smart contract technology. For now there are structured funds, futures, options and various derivatives, as well as new kinds of innovations such as perpetual options and liquidity providers tokens (LP) that are powered by automated smart contracts that have never appeared before.

There are too many types and here we limit the discussion to "DeFi on-chain funds" to facilitate research and discussion, which is defined as follows:

Funds receive capital from investors in the form of mainstream tokens such as ETH/BTC/stablecoins. The funds are operated by the project/fund manager, and all the operations are on-chain. The funds will invest the capital into one or several decentralized finance products, according to the pre-agreed strategy, to realize the appreciation of investors’ assets.

If we expand the details, the projects shall fit the definition below:

Users/investors:

Based on the anonymity and permissionless distinctives of DeFi, any user can participate in the investment of DeFi on-chain funds. However, some funds might set whitelists to limit the number of participants.

Investment and profit:

The goal of the product is that users can achieve capital appreciation via investing into the product itself. The majority of the appreciation shall be mainstream tokens such as ETH/BTC/stablecoins instead of altcoins that are issued by platforms and have higher volatility. In this way the funds are able to capture long-term organic returns through strategies and managements, rather than short-term returns brought by issuance of platform tokens.

About operation authority and scopes:

The authority shall be controlled by smart contracts, and the funds’ assets can only interact with a certain set of smart contracts, tokens and DAppsdapps. The scopes are pre-defined before investment and to ensure transparency and safety, every transaction shall be on chain rather than be put into a CEX for opaque operation.

How big is the market for DeFi on-chain funds?

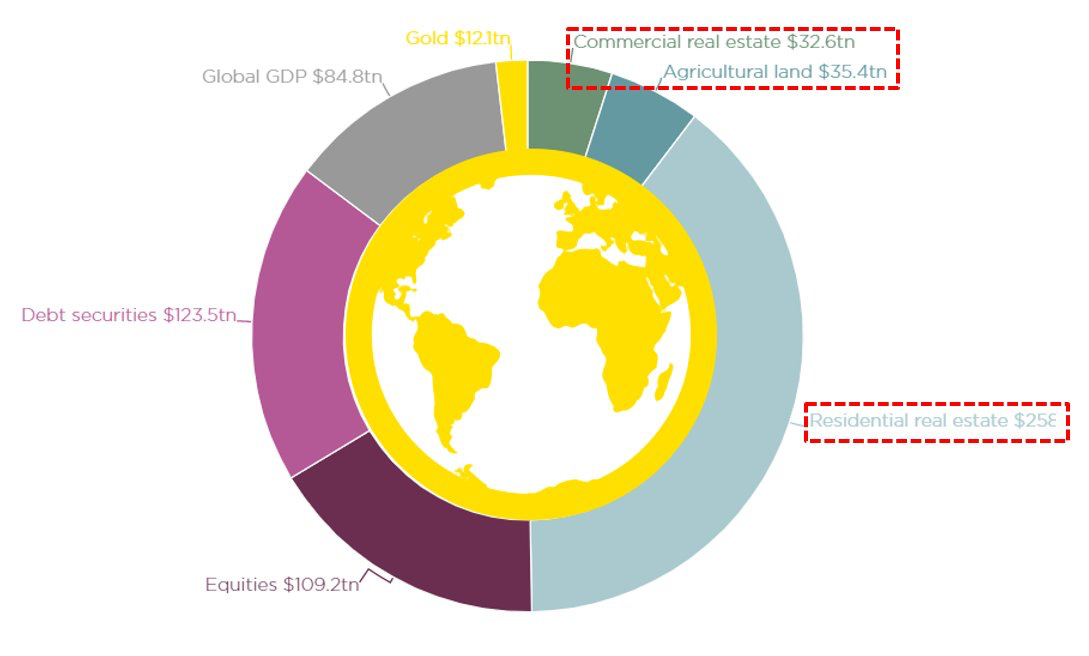

Currently, global funds manage a total of $112 trillion in assets. According to Twitter influencer Alf, the global stock market is $109 trillion, the bond market is $124 trillion, gold is $12 trillion, and digital assets are less than $2 trillion. According to Investopedia data, the derivatives market has a size of about 600 trillion US dollars. If we only consider the crypto market, assuming that 10% of assets are managed by funds, and 30% of them are managed in the form of on-chain funds, then based on the current market value of 1.2 trillion in the cryptocurrency market, there will be $36 billion of assets in on-chain funds. For now, fund volume is much lower than this amount.

Source:

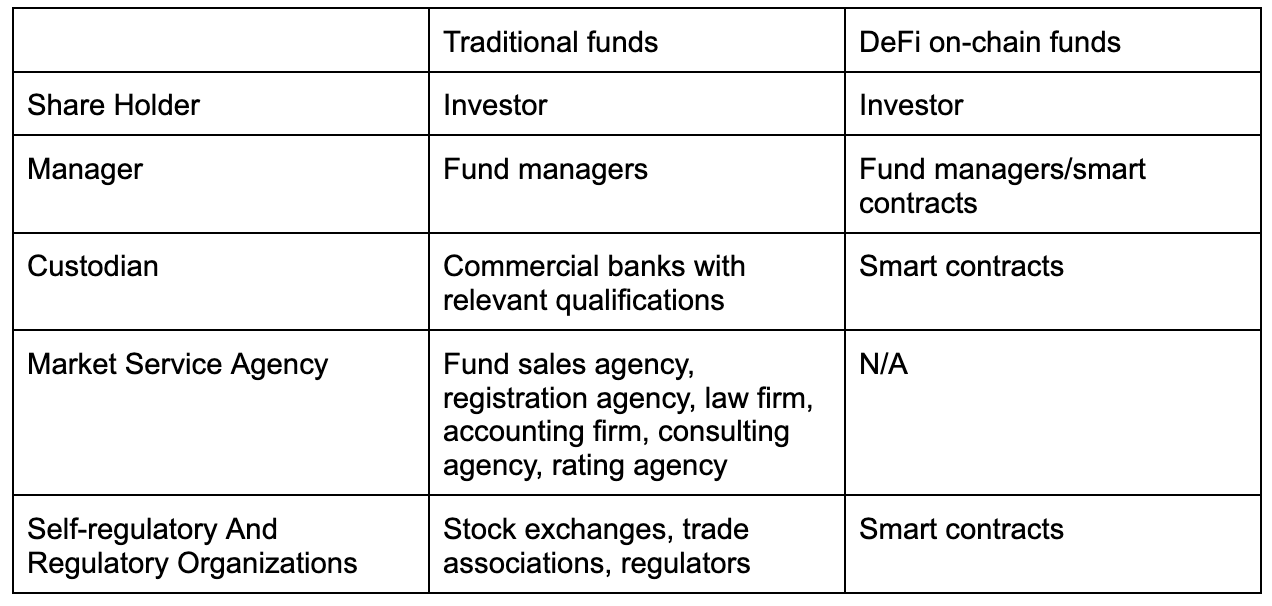

Comparison of the ecological roles of traditional funds and DeFi on-chain funds

Traditional asset management industry has already derived a complete ecological industry chain, including front-end services, back-end ratings and certifications, as well as related laws and regulations, etc. However DeFi on-chain funds have no certification and qualification, no relevant upstream and downstream services in related industries. At present, the only advantage that DeFi on-chain funds have is technical advantages brought by blockchain and smart contract technology, which can guarantee asset transparency and capital efficiency.

Different Types of DeFi on-chain funds

Traditional funds are classified in dozens of ways, some of them are:

Fundraising methods(public/private);

Operation methods(close/open);

Investment concepts(passive/active);

Legal forms(contractual, corporate);

Transaction methods(in-exchange/OTC);

Investment objects(Stocks, bonds, currencies or mixed)

Other classifications

However, whether it’s in DeFi or in the traditional financial field, no matter what asset it is based on or under what framework, the strategy is the most fascinating part, so here we divide our research targets by strategies. This research includes 22 projects that can fit into the definition of DeFi on-chain funds, with multi-dimensional analysis of them.

The categories are divided as follows:

First of all, the product will meet our definition of "DeFi on-chain funds", and then classified into three types according to the specific implementation form of the strategy: algorithmic strategy fund, active strategy fund, and passive strategy fund, the specific definitions are as follows:

Active strategy fund: based on their professional knowledge, fund managers conduct on-chain operations within the scope that are specified by the smart contract. The goal of the active fund is to pursue returns that can exceed the average market performance. Some examples are DeFiEdge Protocol, Arrakis Finance, etc.

Algorithmic strategy fund: Users invest funds, and contracts are automatically executed according to predefined algorithms and strategies to help users build structured asset portfolios or help users perform repetitive operations. Typical products are Yearn Finance and Ribbon Finance.

Passive strategy funds: Mainly index funds, diversify investment in a certain type of assets, or track the performance of certain/multiple types of assets, providing users with extensive market exposure, low operating expenses and low portfolio turnover. Typical products are DeFi Pulse Index (DPI), Metaverse Index, ETH 2x Flexible Leverage Index, etc.

Risk (in general): active strategy funds > algorithmic strategy funds > passive strategy funds

Return (in general): active strategy funds > algorithmic strategy funds > passive strategy funds

Active Strategy Funds: Code is law, contract is regulation

Active strategy funds are relatively easy to understand. Generally, the mechanism of most active strategy funds is to use smart contracts to define the scope of investment. The smart contract will be deployed before the fund opens, and the fund manager can only act within the scope. For example, some contracts only allow managers to borrow/lend from major lending protocols such as AAVE and Compound, or to provide liquidity for certain trading pairs on Uniswap V3.

This type of on-chain funds is more similar to traditional funds, managers earn a certain ratio of management fee and carrys. Currently such funds are relatively small in scale and have huge room for growth.

Algorithmic Strategy Funds: Combining new assets to build powerful on-chain products

Compared with the other two types of DeFi on-chain funds, algorithmic strategy funds are more diversified, some famous DeFi projects like Yearn Finance, Beefy Finance can also be categorized into this type.

Algorithmic strategy funds are the place with huge innovations, combining new types of DeFi assets, such as liquidity providers token, power perpetual, etc, along with other long/short leverage products for hedging, to build financial products that have higher returns and lower risks.

Generally the share of an algorithmic strategy fund can not be traded on open markets, but investors can always deposit and withdraw, or wait for a periodic settlement for withdrawal and deposit.

Passive Strategy Funds: use smart contract to automatically track whatever you want

Generally, passive strategy funds will issue ERC20 tokens to represent the share of the funds, and then the funds’ smart contracts will buy or sell the corresponding assets according to the predefined rules. The platforms will give out governance tokens to attract users to buy index funds, or incentivize users to provide liquidity of the shares in order for others to trade on DEXs.

Most of the platforms allow users to trade shares in the open market, which is similar to ETFs, and users can arbitrage by minting and redeeming shares.

Examples of typical projects

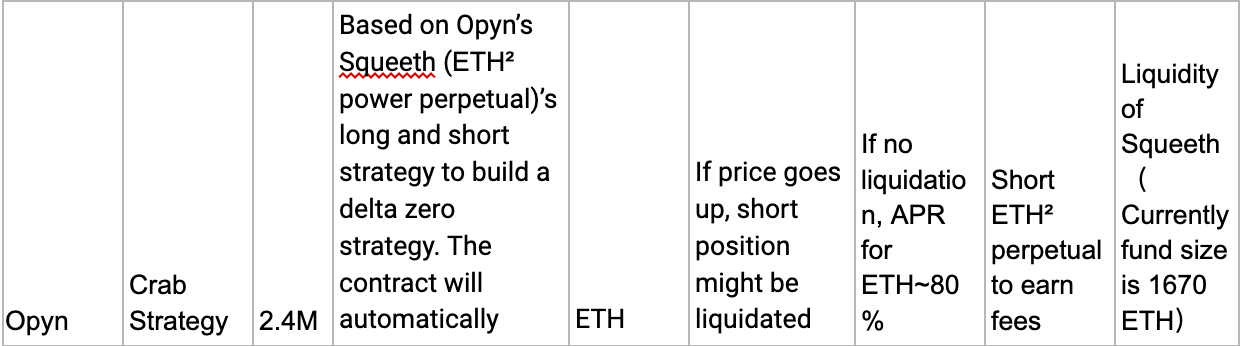

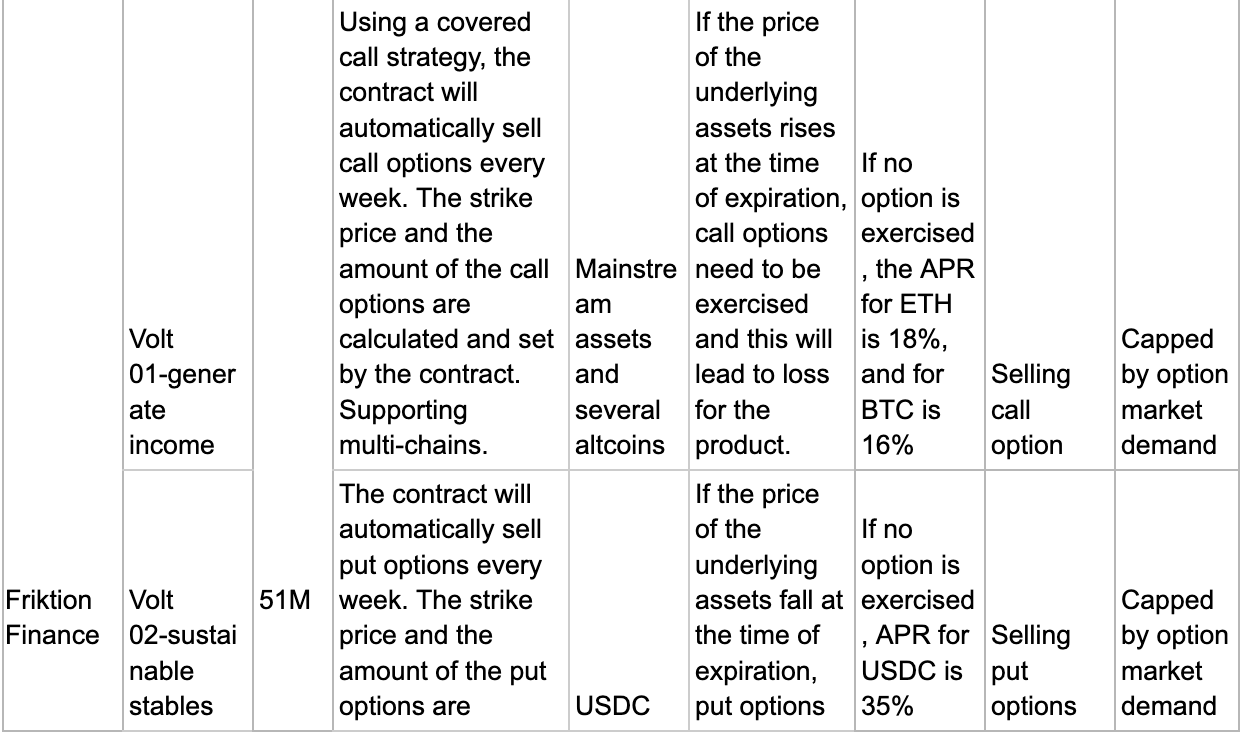

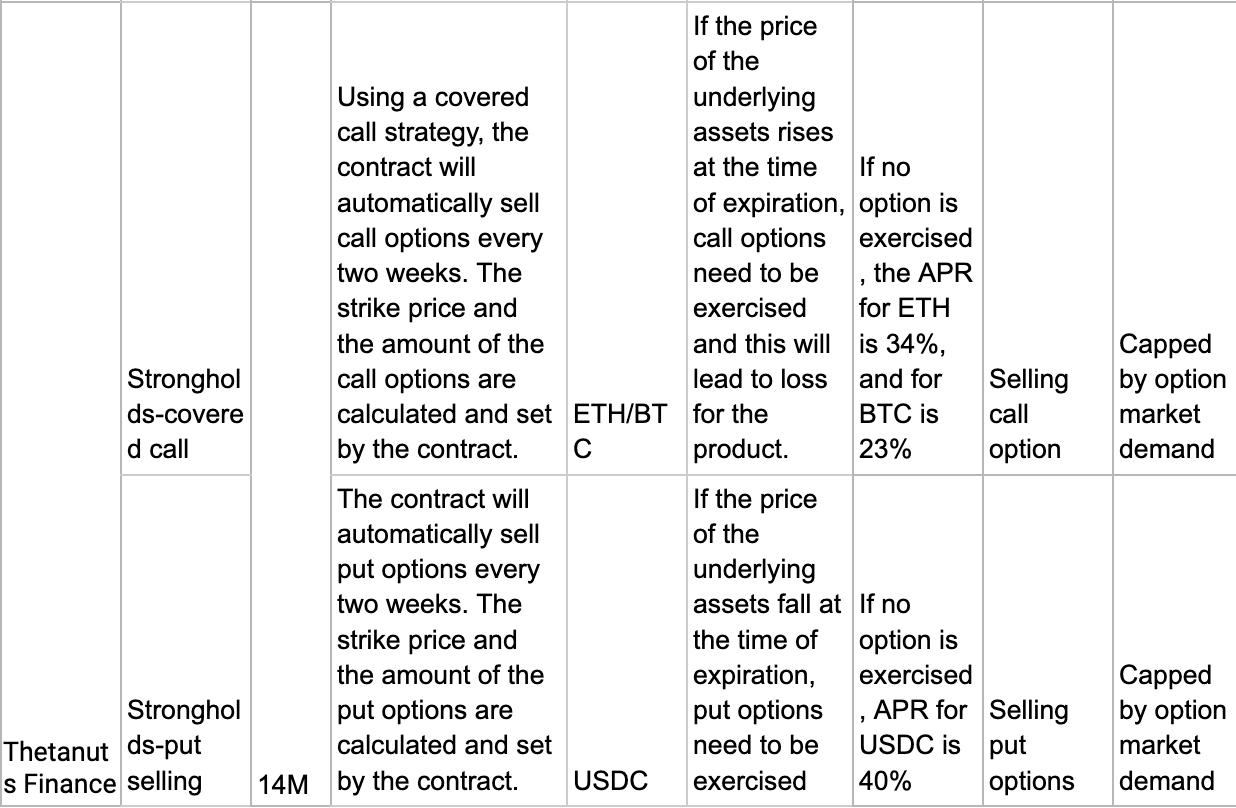

Ribbon Finance - On-chain automatic option strategy

https://docs.google.com/document/d/1yxfUIG5sc_tr9eFma_aZfeaAvxogNlBC6Guoz4Idlpk/edit

Ribbon Finance is a DeFi structured product, based on Opyn’s options. Currently they’ve launched two kinds of strategies: covered call (sell call options on the assets that you already own) and put selling (hold stablecoins and sell put options of other crypto assets). Now Ribbon Finance has deployed its product on three blockchains: Avalanche, Solana and Ethereum. As of early August 2022, Ribbon Finance has an AUM of 70M USD on Ethereum, and it is the largest in terms of AUM among products of the same type.

Investors put money into the fund, then Ribbon Finance’s smart contracts will automatically calculate the strike price and amount of the options, and sell options across several platforms on Friday. Normally all the options get sold in 10 minutes. All the options expire after one week, and when they reach expiration, if no option is exercised, the fund can earn premiums, which is all the profit generated by selling options. Otherwise the fund might suffer some loss, the amount of loss depends on the price of the underlying assets at expiration.

In the future, Ribbon will also release products including futures, fixed income products and other derivatives, to help users improve the risk-return of funds.

Core Products & Design Principle

The core product currently launched by Ribbon Finance is called Theta Vault, which includes Covered Call and Put Selling strategies, with a total of 12 products.

Ribbon Finance's Covered Call is a strategy that holds the corresponding cryptocurrency and sells call options on the cryptocurrency every Friday to obtain premium income. Put Selling is the opposite strategy, holding USDC and selling a certain number of put option combinations every Friday to make a profit.

The strategy takes current market volatility into account by setting a fixed delta value. In Ribbon Finance V1, the team manually calculated the strike price of the option on the basis of delta=0.1. In V2, the contract reads the current spot price from Chainlink and automatically calculates the market volatility, and calculates the strike price in combination with the preset delta value. All options are valid for one week.

In addition, in the latest version, Theta Vault integrates with Yearn Finance, investing idle funds into Yearn Finance to add an additional risk-free return. All operations on Ribbon are implemented through smart contracts, which are one typical algorithmic strategy funds.

Risk and Return

Whether you sell a call or a put, the way to make a profit is in the hope that the option won't be exercised (and thus lapsed) at settlement. Looking at Ribbon's historical performance, options have been exercised (and thus lost) less than 5% of the time since January 2020. Since the altcoin market fluctuates greatly, it is easy to hit the strike price at the time of exercise, and the funds that have suffered losses are mostly covered call strategies of altcoins.

On the whole, without extreme market conditions, Ribbon Finance can indeed help users gain token appreciation. Theoretically, if all the options are not exercised, on Ribbon Finance, the APR for ETH is 34%, for BTC is 27%, and for USDC is 50%. But in reality, considering the huge volatility of the crypto market, the overall return is not ideal. The year-to-date return for BTC strategy is currently 6.05% and ETH strategy is 3.38%, while USDC strategy has 28% total loss.

Considering the Ribbon product mechanism design, the Covered call strategy is more suitable for bear markets, avoiding call options with rapid price rises from being exercised, and gaining some token returns. While in the bull market, USDC's put selling strategy is suitable to avoid the rapid price drop and the put option being exercised.

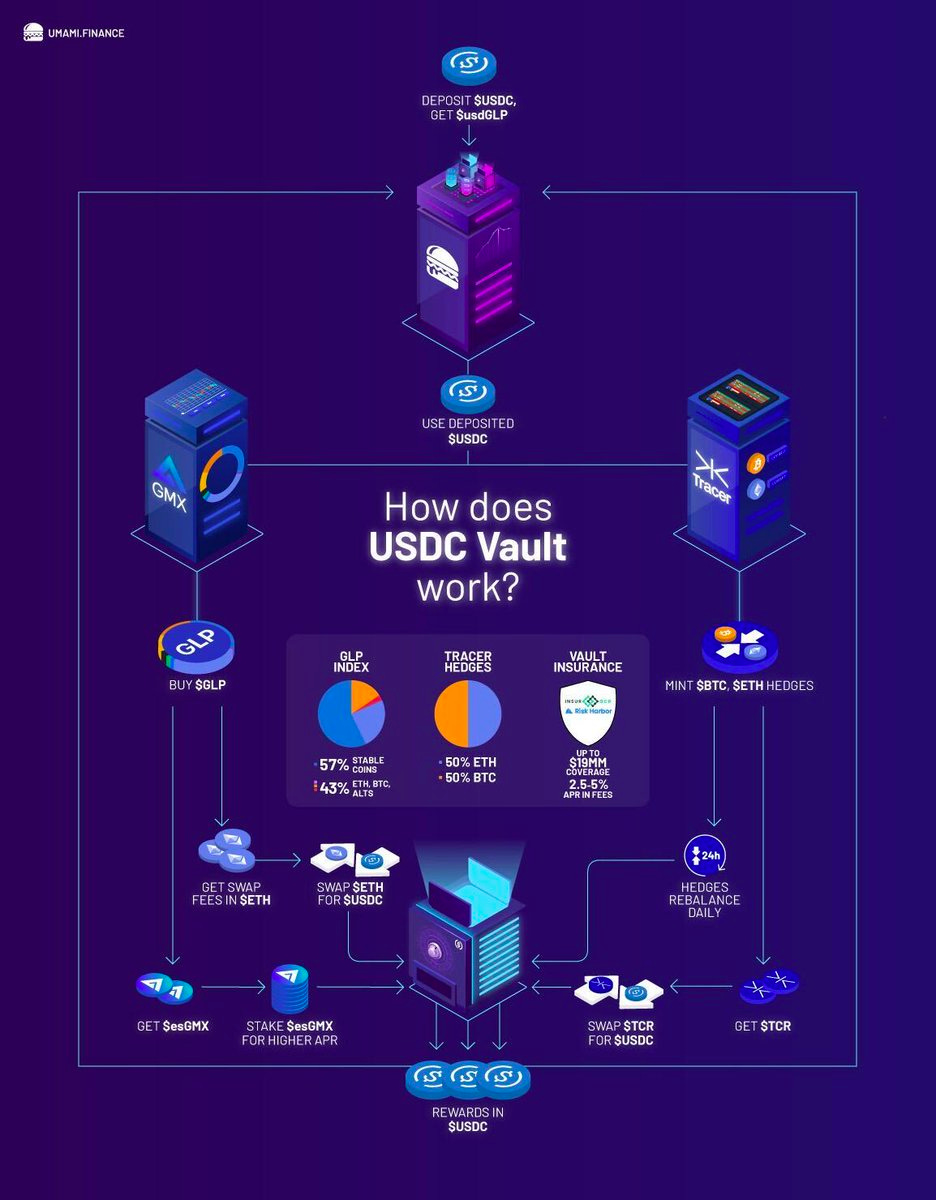

Umami Finance - Based on innovative DeFi assets to build a hedge fund with great risk-return

https://docs.google.com/document/d/1xFyKV04C_ShZC85D-h-hFfIH1BYqiPPx6l_SGfq_Xh8/edit

On August 19th, due to market volatility, Umami Finance closed this vault and returned all the funds to investors. The reason is that Mycelium (previously called Tracer DAO) perpetual pool tokens do have deviation when the market fluctuates wildly. When Umami used Mycelium’s perpetual pool token to hedge the price downside risk, the return from short position cannot cover the loss on their long position. And finally they decided to close the fund. But anyway the product design is pretty innovative and worth a deep research.

Umami Finance is the first decentralized reserve protocol (similar to Olympus DAO) on Arbitrum. Last month Umami Finance released a USDC fund based on GMX’s GLP, and used Mycelium’s perpetual pool token to hedge risk, to give investors a yield of 20% APR.

Source:Umami Finance Docs

The DeFi LEGO module: GMX’s GLP and Mycelium’s Perpetual Pool

GMX is a decentralized perpetual contract exchange on Arbitrum and Avalanche. GLP is the generalized liquidity provider that acts as counterparty on all the trading scenarios. Trading on GMX has no slippage, but is directly exchanged at this price according to Chainlink's quotation. The counterparty funds for the swap come from GLP and the upper limit will be set according to the size of the GLP pool.

Source: GMX, here MAX ETH in and MAX USDC out is the trading size limit set by the platform

Meanwhile if the trading size increases, the fee will also increase from 0.3% to 0.8%.

The GLP is provided by the user and contains a basket of asset combinations, the ratio of which is set by the platform. Users can use any of the assets in the basket to mint GLP, in order to maintain a stable proportion, users will have to pay a fee in the process of minting, by adjusting the mint fee the platform incentivize users to mint GLP with missing assets to maintain the balance of the GLP pool. For example, when the amount of WBTC in the GLP pool is much lower than the set ratio and ETH is higher than the set ratio, users will incur additional fees for using ETH to mint GLP, and the fees for using WBTC to mint will be lower.

70% of the proceeds from trading, minting and destroying GLP, leveraged trades and liquidation activities on the GMX platform (collectively referred to as platform fee) are allocated to GLP in the form of ETH. The remainder is allocated to the governance token GMX.

Since GLP consists of a certain proportion of crypto assets, the net value of GLP units will also fluctuate with the token price. The chart below shows the composition of the GLP.

Composition of the GLP.(2022.08.07)

Source: https://www.gmxstats.com/

GLP Net Change Curve (2022.08.07)

Source: https://www.gmxstats.com/

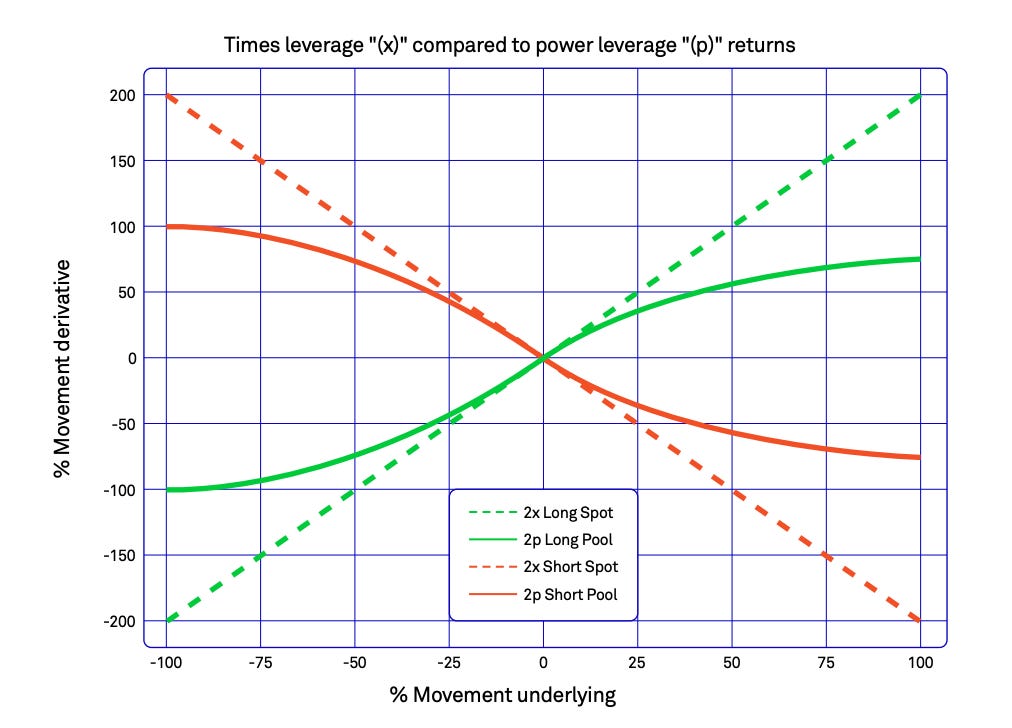

Mycelium (formerly known as Tracer DAO)’s Perpetual Pool

As an example, Mycelium has built 3x long and 3x short tokens that allow users to directly mint long or short tokens using USDC. Mycelium periodically adjusts the ratio between the two pools based on the price of Ether. Assuming a 1% increase in the asset price, the triple leverage pool will automatically transfer 3% of the funds from the short pool to the long pool when adjusted, and vice versa. Thus it builds a leveraged product that will not get liquidated.

The adjustment of the pool is based on the following curve (the graph shows 2x leverage as an example), with the horizontal axis being the price movement of the underlying asset and the vertical axis being the amount of money transferred from the pool. You can see that the greater the price movement, the more difficult it is to adjust the leverage precisely.

In addition, an arbitrage model is used in the middle to keep both sides of the pool balanced, as well as to withdraw a certain amount of fees for triggering contracts to achieve a stable operation of the product.

Umami’s strategy:

As you can see above, GLP contains about 40+% volatile assets (mainly BTC and ETH, plus tokens like UNI) and 50+% stable assets (mainly USDC). Therefore, buying GLP is equivalent to holding this basket of assets, with future cash flow income from GMX platform fees. So Umami's Vault uses Mycelium's triple leverage tokens to short BTC and ETH position as a hedge for the volatile assets portion in proportion to their size (Mycelium only supports ETH and BTC, but already covers most of them) to get a stable return. The contract is adjusted once a day to ensure the hedged amount is accurate.

In addition, a small amount of funds is spent on GLP insurance from the insurance platform insurance to protect against unexpected losses due to hacking, etc.

For the detail of the insurance: https://app.insurace.io/Insurance/Cart?id=124&referrer=545066382753150189457177837072918687520318754040

Risk and return

Umami actually takes into account almost all kinds of risks, including insurance and risk harbor to protect GLP from unexpected security incidents; and the use of Mycelium to hedge the risk of GLP. However, due to the underlying product mechanics, there are still risks, some of them are:

Risk from Mycelium: Mycelium does rebalance every 8 hours to allocate long/short pool ratios to maintain leverage, but Mycelium's curves are approximate simulations and Mycelium does not guarantee a completely even pool allocation in the event of large price fluctuations.

And other contract-related risks arising out of Mycelium. Umami's insurance does not currently cover the potential risk from Mycelium.

If a large GLP withdrawal or deposit causes an imbalance in the GLP ratio, Umami incurs an additional cost for every 9 hours of rebalance.

According to the current state, the amount of rebalance every 9 hours is about 1% of the fund. The fees from all those rebalance processes might be around several points of the total amount, and this will significantly reduce the revenue. If GLP’s ratio is uneven then there might be higher cost when mint or burn GLP.

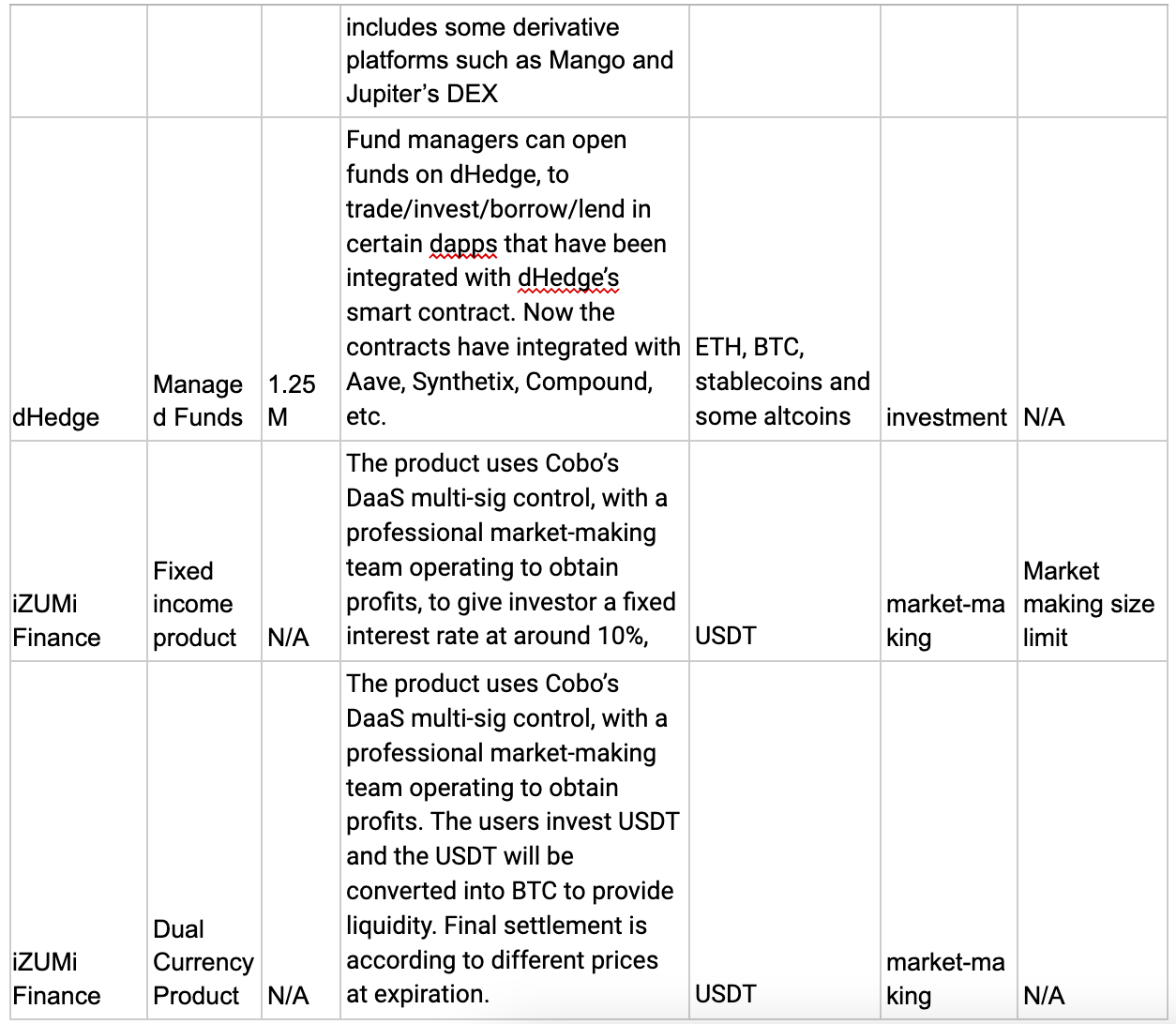

iZUMi Finance: Closed-end active funds operated by professionals

https://docs.google.com/document/d/1bsaxgztJtk8ciXW8BfBlkz55RyhWEKsTEkC_zesUR0E/edit#

iZUMi Finance is a multi-chain one-stop liquidity service platform that offers a variety of products around liquidity services, including liquidity box, a liquidity incentive tool, and iZiswap, an efficient decentralized exchange. iZUMi Finance will soon launch three products, namely fixed income bonds, dual currency finance, and impermanent loss insurance.

Both fixed income bond product and dual currency product can be defined as DeFi on-chain funds - active strategy funds. Compared to the various fund products mentioned earlier, iZUMi Finance offers closed-end funds that cannot be traded after purchase and can only be redeemed with interest after maturity.

iZUMi Finance fixed income product

iZUMi Finance fixed income bond product is implemented through the Gnosis multi-signature wallet. Permission control is implemented through Cobo DaaS multi-signature controls, allowing a party to perform actions within a predefined scope, such as trading and adjusting the price range of the position on Uniswap V3.

iZUMi Finance offers a 30-day bond product, provides a 10% annualized yield on USDT and pays principal and interest at maturity. The bonds are raised to provide liquidity on a decentralized exchange, with a professional trading team providing the strategy.

The multi-signature wallet is jointly managed by iZUMi Finance and two partners, and is open only to the market maker (MM) team to provide liquidity and adjust the price range on Uniswap V3. The funds are withdrawn by all three parties at the end of the day with the co-signature. The bond proceeds are a fixed 10% APR and the rest of the proceeds go to the Market Maker. If the proceeds are insufficient, the Market Maker makes up the rest with its own margin.

iZUMi Finance dual currency product

Another financial product from iZUMi Finance is a dual currency product, which offers a slightly higher risk and return compared to bond products. The product is invested in USDT with an optional 1/7/30 lock-in period, and the funds are used to provide liquidity on the BTC/USDT pair on DEX.

The final asset returned by a dual currency product is determined by the market price. A price range is set at the time of product purchase and the contract will automatically trade a% of USDT as BTC on DEX at market price at the time of investment to form liquidity and earn trading fees within a certain price range.

If the price stays within the price range at the time of redemption, the user withdraws the liquidity corresponding to the principal amount and receives 50% to 150% APR of the proceeds. If the price is higher than the set price limit, the user receives the value of liquidity tokens above the price range in the form of USDT. If the price is below the set price floor, the user will receive the value of liquidity tokens below the price range in the form of BTC.

Compared to other active strategy funds, apart from maintaining the safety and transparency of on-chain funds, iZUMi Finance's products are more flexible through the operation of a professional team, and are relatively more competitive as they can provide stable, largely unrelated to market bull and bear returns.

iZUMi Finance impermanent loss product

After receiving Uniswap V3’s liquidity provider NFT, the user stakes the NFT in the smart contract of iZUMi Finance's impermanent loss insurance product, which automatically calculates the amount to be hedged and the related costs, for a period of 30 days. The contract will automatically apply a portion of the fee income to the purchase of the insurance. iZUMi Finance will use API to open a position in CEX using a combination of hedging strategies. Settlement is made when the insurance expires or when the liquidity leaves a set price range, paying the user's premium. With impermanent loss insurance, the user is able to avoid impermanent loss by providing liquidity, thus earning a stable market making fee income.

All three of iZUMi Finance's products are innovative attempts. The first two can be categorized as DeFi active-strategy on-chain funds, and the insurance product combines the CEX strategy, but the calculation and payment of impermanent loss and amounts are transparently available on the chain. Those products will launch soon under the name of Glass Finance, which iZUMi Finance is currently involved in incubating. Glass Finance has joined the first phase of Cronos Accelerator and is looking forward to the product launch soon.

Advantages of DeFi on-chain funds

Asset transparency and security: Asset operations are fully traceable on the blockchain, reducing under-the-hood operations. Whether it is active, passive, or algorithmic strategy funds, all the transactions involved are fully traceable on the blockchain in real time. And most of the funds can achieve exit at any time, users' assets can be better protected.

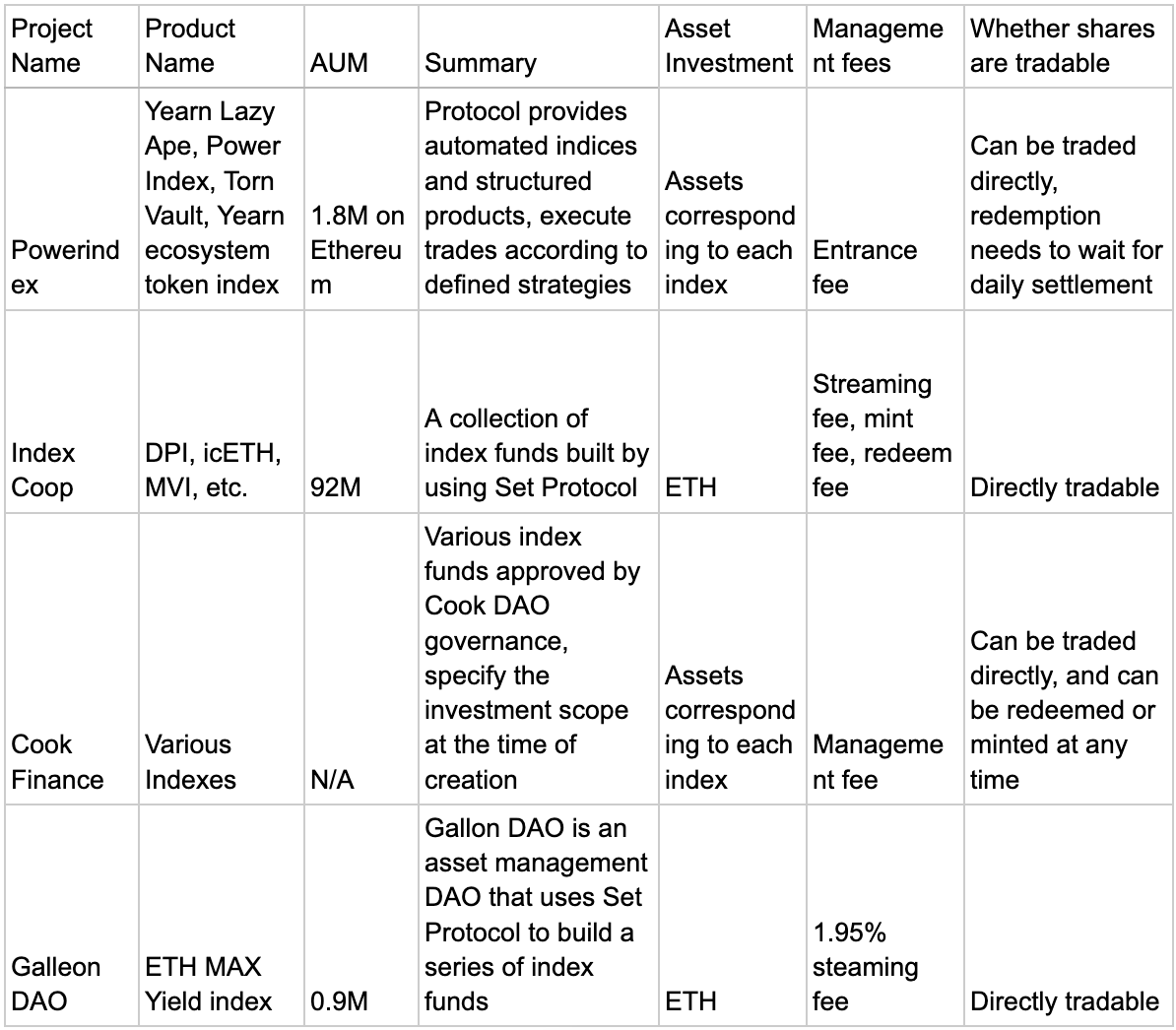

New asset composability: Thetanuts Finance, Index Coop, Cook Finance and other on-chain funds issue corresponding ERC20 tokens representing fund shares, which can participate in other Staking activities and even work as collaterals to participate in lending activities in the future.

Diversification of investment targets: Traditional funds only allow funds to invest in permitted asset classes, such as currency, equity, and bond, in consideration of risk control; DeFi on-chain funds are able to invest in more diversified targets, including interest bearing token, perpetual contracts, leveraged tokens, liquidity providing tokens, etc. The combination and hedging of different new products results in a low-risk, high-yield (over 20% yearly return) product that is close to Delta Neutral. These kinds of products include a certain amount of risk, but have a stable source of return with a manageable risk compared to Luna's Anchor Protocol, which offers a stable return of about 20%.

Disadvantages of DeFi on-chain funds

Overly transparent: vulnerable to malicious counterparty attacks. Take GMX’s GLP as an example, counterparties might deposit huge amounts of certain tokens on purpose to bias the ratio and raise the mint fee, to add extra expense for Umami’s USDC vault. Also, layers of assets are nested, which can easily accrue risk.

High operating expenses: Some of the fund products with automatic running strategies require frequent on-chain operations, resulting in high fee expenses.

Inaccurate calculation: DEX using AMM has difficulty in making accurate estimates of results during the trading process. In addition, design curves such as Mycelium, which simulate leverage, can also have large deviations when the market is highly volatile, resulting in additional losses and expenses for the fund.

Risk on contract level: On-chain fund products are often a combination of multiple assets, associated to multiple smart contracts. Also the funds are kept in the smart contracts. If one of the contracts gets hacked, then it can have an impact on the entire fund. Umami Finance’s USDC vault even uses part of the fund for insurance.

Product complexity: Compared to centralized financial products, DeFi fund products still have a high barrier to understanding and entry. It's not just that DeFi products have a small user base and are complex and difficult to use, but also that they have various kinds of products that have no general standards. For example, to understand the principles and risks of the Opyn Crab Strategy, one needs to understand the principles of products such as power perpetual contract and Opyn’s Squeeth.

Innovative products are not yet stable and need to be tested over time: Umami Finance uses Mycelium's leveraged tokens for hedging, expecting to be able to hedge volatile asset positions in GLP without the risk of liquidation. However, Mycelium's mechanism is designed to perform adjustments every 8 hours, which can easily lead to deviations when the market is highly volatile, leading to significant losses in Umami's USDC Vault on Aug 18-19. In the end, Umami decided to close the Vault and compensate for the shortfall with the team's funds. Innovative products such as these using on-chain algorithms still have large, unproven risks that need to be tested over time.

Trends and opportunities:

Platforms are designing their own fund products: During our research, we found that DeFi trading platforms are developing their own platform-based financial products, packaged as fund products that users can simply understand the existing risks and returns, without the need to operate them themselves. Typical example is the Crab strategy built on Opyn’s Squeeth.

Combining DID will be the future direction of active strategy funds: In an anonymous environment, even with smart contracts to secure funds, it is difficult for users to trust active strategy fund products. Most fund projects, such as DeFiEdge, are relatively early, and the platform itself does not provide sufficient credit backing to fund managers. Some of the projects adopt the way of Twitter account association, which has relatively limited effect. If the DID can be combined with the actual performance of the fund manager's historical returns on the chain, and if it can be confirmed that it is indeed the fund manager who is actually operating the fund, it can give the product more credibility and has the opportunity to derive fund ratings in an anonymous environment.

The need for stable liquidity for platforms: Platforms such as GMX and Uniswap want to have sufficient and stable liquidity, and funds such as Umami Finance and DeFiEdge can help provide long-term, stable liquidity for DEX. In addition, for Umami Finance's products, the combination of liquidity and leveraged tokens for hedging provides users with a high yielding financial product that essentially benefits all four parties (Umami Finance, GMX, Mycelium and investors).

Fund marketing channel opportunities: with wallets as the entrance, or similar to traditional brokerages’ business model, to integrate other financial service onto their website, it is possible to horizontally compare the returns and risks of various on-chain funds, helping users to reduce decision costs, and also to channel the flow of reliable DeFi on-chain fund products.

Conclusion

Overall, DeFi on-chain funds are still a track with untapped potential, and the overall AUM is relatively small currently. However, innovative products, such as Umami's USDC Vault and Opyn’s Crab Strategy, continue to be in short supply, indicating that market demand does exist. High market volatility and speculative activity are all conditions that emerged early in the market, and there are also a number of on-chain fund products that are facing problems due to poor market conditions and infrastructure.

Compared to the traditional fund model, the standards, operational processes, models, and ecological roles of on-chain funds are still at a very early point, and many ecological roles are even missing. We look forward to seeing more builders emerging in the future with more exploration and ideas to build a more robust DeFi ecosystem.